On May 10, 2023, the Marketing Accountability Standards Board (MASB) released its briefing, Bud Light ‘Boycott’ May Not End, Here Is Why. It opined that the travails of Bud Light which began in early April were not a consequence of a traditional boycott. Rather, Bud Light faced a much more permanent “brand divorce” whereby previously loyal consumers changed their brand preference – in many cases permanently – away from Bud Light.

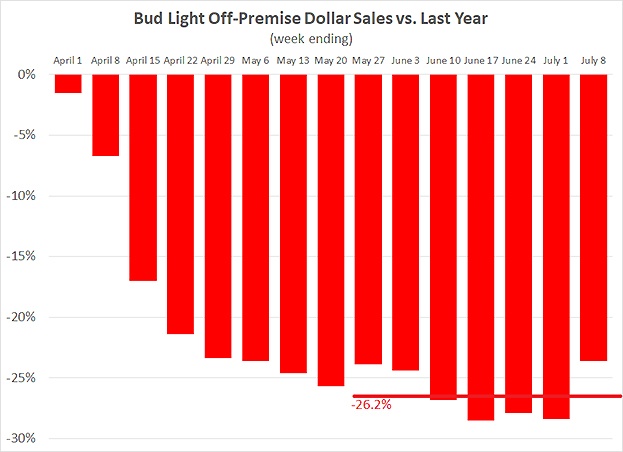

An updated chart (Exhibit 1, below) from our first publication illustrates Bud Light’s continuing struggles. For the seven weeks spanning the category-important Memorial Day through Independence Day time period (weeks ending May 27 through July 8), Bud Light off-premise sales averaged a 26.2% weekly drop versus the same period the previous year. And, as we will explain, this latest trend is much worse than it appears on the surface.

Exhibit 1

We previously surmised a high probability that Bud Light would price-promote aggressively over Memorial Day. Even we were surprised at the magnitude of their aggressive promotions. Rebates of $15 on multi-packs proliferated across the country. In some instances, the net impact was the consumer being paid to take beer.

In the chart above, the sales numbers for the weeks subject to the rebate would not factor in these rebates, which are processed independently of the register transaction. This particular offer extended through July 11, thereby including the second major beer holiday of the summer, the 4th of July. While we understand the predicament faced by the brand, these efforts to “buy volume” can lead to a brand-value death spiral. We believe this is likely already underway.

How the MASB Brand Investment & Valuation Model Supports This Conclusion

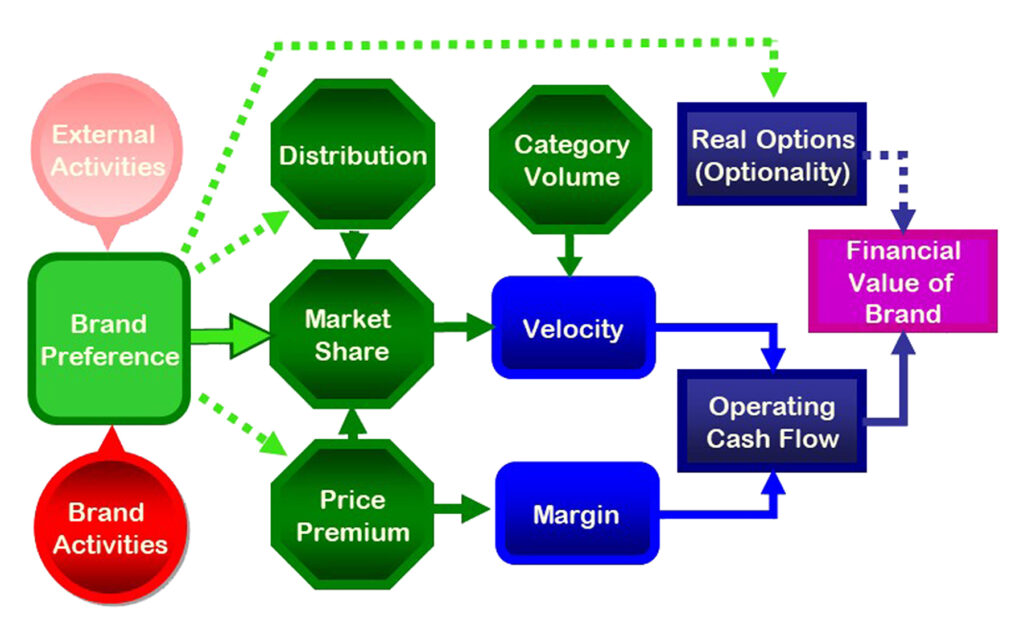

Why did MASB see this coming and why do we believe that Bud Light’s future is extremely challenged? The foundation of our conclusions resides in MASB’s Brand Investment & Valuation (BIV) model which was initially published in 2018 and subsequently refined in 2021. The 2021 model is shown in Exhibit 2 below. Each element of this model has played out already or will likely play a role in Bud Light’s future.

Here is how we see each of these elements impacting the Bud Light situation.

Exhibit 2: MASB Brand Investment & Valuation Model (2021)

Brand Activities – Every brand marketing and selling activity impacts brand preference. Large-scale marketers, such as Bud Light, heavily focus on so-called “tent-pole” marketing events (e.g., exclusive Super Bowl television spots, typically enhanced with digital and social media reinforcers). However, we have now seen a much smaller-scale marketing activity creating a very sizable impact, and the downside risk increases when the messaging does not connect with the core high-usage consumer. While the more recently released television and online video ads are more aligned with Bud Light’s traditional creative approach, their ability to influence these core consumers is still being blunted by the controversy.

For example, AB InBev released its “Easy to Summer” 60-second ad for Bud Light on June 22. This ad is reminiscent of traditional Bud Light ads, featuring humorous slapstick moments of everyday people enjoying the product.

Quoting from MASB’s The Financial Value of Brands Imperative publication: “External activities, such as competitive advertising and social media conversations, also influence preference for the brand.”

These external activities can be somewhat scary to the marketer, as they are largely outside of the marketer’s immediate control. In Bud Light’s situation, social media activities initially fanned the flames of consumer discontent. As of now, the social media channels remain a hostile environment for Bud Light. As an example of the intensity of the negativity on social media, from April 2 to June 21 only one tweet remained posted, a very simple and innocuous “TGIF?” Yet it still received 33,400 comments, mostly negative and meme-filled, to 5,350 likes.

Exhibit 3: Bud Light “TGIF?” Twitter Post

This type of online response will continue to hamper all brand activities (advertising, promotions, events, sponsorships, etc.) making it difficult for the brand to leverage these avenues. Even simple event announcements with the chance to win free tickets are facing these negative comment difficulties (see Exhibit 4, comments not shown here due to content).

Exhibit 4: Bud Light “Backyard Tour” Twitter Post

In the MASB BIV model as shown, external activities and brand activities drive brand preference. It is the combination of these two inputs, for better or worse, that influences the direction, depth, and resilience of brand preference, which, based on its extensive research, MASB views as the cornerstone metric of explaining and predicting marketing outcomes. For more details on the power and use of brand preference, please see these MASB resources: Brand Investment and Valuation: A New, Empirically-based Approach and Five Compelling Reasons to Use Brand Preference.

This simple but impactful formula may be the most important framework that explains Bud Light’s predicament while also foreshadowing what is likely to come. While it would be naïve to deny that both right-leaning and left-leaning political constituencies have weighed in on the Bud Light situation and in some cases provoked consumer discontent, it would be equally naïve to ignore that many non-politically aligned consumers have simply abandoned the brand. This is the financial sledgehammer of a brand divorce. In a traditional boycott, there is an exit ramp, a path to re-engagement. In these cases, the customers boycotting the brand still prefer it to competitors, they are just withholding their purchases until a set of demands is addressed. The managers of Bud Light may not be afforded such an exit ramp. In fact, we do not believe there is one in the near term as many of the customers who left the brand have changed their preference to others and Bud Light’s competitors are using the corresponding windfall to reinforce this preference for their brands through their own marketing activities. Given this reality, any Bud Light recovery will require significant positive influences from both External Activities and Brand Activities. Merely hoping that things revert to the old norm would not seem to cut it.

On the other hand, if Bud Light did not have the strong preference that it did prior to the controversy, it would not be in a position to stage a recovery. It is only because of the preference built up over decades of marketing-driven positive brand associations that it still has a viable business today. Weaker preference brands would have completely failed.

The BIV model has a large arrow from Brand Preference to Market Share, which Exhibit 2 illustrates. As has been widely published, Bud Light’s share losses have most significantly benefitted its largest competitors in the low-calorie segment, Coors Light and Miller Lite. And Constellation Brands’ Modelo Especial recently overtook Bud Light in the United States as the top dollar-share beer brand. [1]

Returning to the BIV model, the previously mentioned $15 rebate program demonstrates the polar opposite of Price Premium, primarily resulting from a rapid decline in retail-level Velocity. As we state in the Financial Value of Brands Imperative publication, advantageous pricing to the marketer “may manifest itself either in the purchaser’s willingness to pay more or the purchaser’s acceptance to pay a non-promoted price versus a discounted price.” When a brand has increasing preference in market, it can choose to take the corresponding benefit in the form of greater market share, higher prices, or a combination of the two. On the other hand, decreasing brand preference drives hard choices in the other direction, decreased share, lowered prices, or a combination. In the case of Bud Light, it is a combination. While complete data has not yet been released, anecdotally it can be expected to be a 20% or greater drop in volume share and a similar drop in price, considering the trade promotions including rebates.

Relating to Distribution, stories have already circulated about Bud Light distribution being removed from certain on-premise trade locations as well as smaller-scale off-premise stores. In the beer industry, larger-scale off-premise distribution is much “stickier” in that it is historically adjusted only twice a year, primarily in spring and secondarily in fall. That said, Newsweek recently wrote about indications that Costco outlets may be discontinuing certain Bud Light packages. [2] We suggest that Bud Light’s misfortunes will likely be amplified by a fuller-scale fall reset of distribution points in the larger-scale off-premise trade. At the very least, this will further cement the losses already experienced by the brand.

Margin is the financial lifeblood of a consumer products enterprise, and we expect AB InBev’s second quarter results scheduled to be released in early August will reflect a margin bloodbath in the United States business which will negatively influence Operating Cash Flow.

Uncertainty remains in the model with respect to Category Volume and Optionality. Published information to this point suggests that beer category volume has held its ground with Bud Light losses shifting to segment alternatives such as Coors Light, Miller Lite, and Yuengling Flight. MASB sees a caution flag, however, in that just as the market-share leader in a category tends to lead category expansion, the opposite can also be true on the downside. We suggest this is a “watch list” item as the next months proceed, but we do not see it as inevitable, in part because the segment alternatives will gladly participate in their newfound wealth. An impediment for them could be the capacity to produce sufficient volume through the summer, so watch for stories of retail-level stockouts as an indicator.

We view Optionality, on the other hand, not as a yellow caution flag for the industry but as a waving red flag for Bud Light. Once again, our FVB Imperatives publication defines optionality as “opportunities to leverage investments in a marketing asset, such as a brand name, customer franchise, or distribution network… in the case of a brand, it is the use of the brand name beyond the initial covered products through a brand or line extension.”

The “Bud Light” moniker has been used frequently in the past on products such as Bud Light Lime and Bud Light Seltzer. Those days seem ancient history at this point. Optionality as a leverage point seems no longer viable. Will Modelo capitalize in some way on optionality? Let’s watch for that. The canary in the coal mine on optionality will be the trends in Bud Light and the competition’s merchandise such as apparel and glassware.

Of course, from MASB’s perspective, all of the preceding commentary would be unnecessary small talk were it not for the impacts on Financial Value of Brand, which becomes the critical linkage to Enterprise Value which is discussed at length in the Imperatives publication. From our May 10 briefing, Exhibit 5 below is an updated chart showing AB InBev’s (ticker BUD) stock price falling and Molson Coors (ticker TAP) advancing, both in absolute terms and relative to the benchmark Dow Jones Industrial Average (ticker DJI). We expect that the major Brand Valuation firms will do deeper dives into the brand value of Bud Light and Budweiser in their upcoming brand valuation rankings. This will provide a deeper look into these outcomes.

Exhibit 5: Stock Price Trends of AB InBev, Molson Coors, and Benchmark

Some additional thoughts

We also wonder if this scenario suggests something more broadly about the brand-connected consumer. Brand-connected consumers may very well have hit a tipping point of strongly rejecting any attempt to be socially engineered from afar, especially when these efforts do not appear “authentic.” That a brand holds true to its roots and acts authentic is Branding 101, especially in the context of sponsorship and influencer marketing. [3] [4]

And authenticity has a long resume in the history of low-calorie beer. Think back to the early Miller Lite All-Stars advertisements and the classic “Great taste…less filling” tag line. In 2014, when Miller Lite reverted back to its original (and arguably “more authentic”) primarily white packaging, they experienced a step change in sales volumes when the switch occurred. Think about Coors Light’s Rocky Mountain Cold Refreshment and the Silver Bullet. Bud Light itself leveraged authenticity through its use of humor in decades of Super Bowl ads. Perhaps a nod to this authenticity angle is the curious improved sales performance of Yuengling Flight, their 95-calorie entry in the low-calorie beer segment. [5] In the case of Bud Light, the brand team must find a way to reestablish the authenticity of the brand in the hearts and minds of consumers. Of course, this is much easier said than done.

Another major economic impact on which we have seen little coverage is that on the enterprise values of hundreds of independent beer distributors across the United States. The brands benefiting from Bud Light’s losses — predominantly among them Coors Light, Miller Lite, Yuengling Flight, and Modelo Especial — reside with the same independent distributor in many local geographies. These distributors’ brand-value windfall comes at the expense of the neighboring AB InBev distributor. Similar is the situation faced by independent bottle manufacturers servicing AB InBev brands. Amid the declining sales of Bud Light, the Irish company Ardagh announced [6] they were closing bottling plants in two Southern U.S. states and laying off approximately 600 employees.

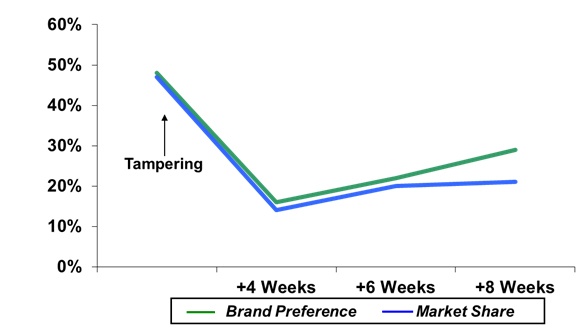

Despite these circumstances, the marketing accountability literature does include a few examples of brands recovering from similar levels of losses. The most dramatic example is that of the Tylenol tampering incident. Brand preference plummeted 32 points as the nation watched several people die from the poisoning. Public sentiment was that the Tylenol brand could no longer be trusted. As brand preference dropped, Tylenol’s market share fell a corresponding 33 points. As Johnson & Johnson addressed the situation responsibly, the strength of the brand’s previous contract (trust) in the minds of consumers was rebuilt, although a bit more slowly than it was damaged (See Exhibit 6).

Exhibit 6: Tylenol Tampering Case Study

It is conceivable for Bud Light to stage a recovery, but time is running out for the brand team to rebuild positive associations for the brand and reverse the downward spiral. As their former customers use the competitors’ offerings, they will be building associations and, ultimately, ingrained preference for those brands. If they can regain even a portion of these customers, it will be one of the most dramatic brand preference turnarounds ever seen. At this point, a continuation of the brand divorce over the near term is much more likely.

PLEASE LEAVE YOUR COMMENTS ON OUR LINKEDIN POST

References

[1] Reuters: Modelo Especial tops Bud Light as most-sold US beer for second consecutive month, July 10, 2023.

[2] Newsweek, Photos Show Bud Light With Costco ‘Death Star’ Amid Plummeting Sales; Giulia Carbonaro, July 11, 2023.

[3] MSI, Fit and Authenticity in Sponsorship and other Horizontal Marketing Partnerships; Bettina Cornwell, August 1, 2019.

[4] MASB, Sponsorship Accountability Part 2: Sponsorship Strategy and Brand Fit; Pace, Ebben, Christensen, October 30, 2019.

[5] New York Post, Yuengling attempts to scoop up Bud Light customers with red, white and blue cans; Shannon Thaler, May 9, 2023.

[6] Independent.ie, Two Ardagh glass bottle plants close amid Bud Light backlash; Samantha McCaughren, July 15, 2023.

About MASB

The Marketing Accountability Standards Board is the acknowledged expert body on the topics of brand evaluation, brand valuation, and marketing return on investment. ANSI, the American National Standards Institute, has designated MASB to serve as the U.S. representative to the ISO technical committee charged with setting global standards on such matters. MASB’s game-changing initiatives are elevating the CMO to their rightful place in the boardroom by making marketing accountable.

The Authors

Frank Findley is a data scientist and Executive Director of the Marketing Accountability Standards Board (MASB) where he represents the U.S. in the creation of international (ISO) marketing standards. His previous work at ARS group, comScore, and MSW Research resulted in improvements to ad testing, tracking, media planning, and competitive intelligence systems. He is a coinventor of the patented Outlook media planner. Findley’s research has appeared in numerous publications including the Journal of Advertising Research, Quirk’s, Forbes, and the books Accountable Marketing (Routledge, 2016) and Master of Marketing Measurement: Margaret Henderson Blair on Marketing Accountability (Cambridge Scholars Publishing, 2021). He was presented the 2021 ARF Great Minds Award for Best Practitioner Paper. He is a regular speaker at marketing industry conferences and a participant on industry boards. Findley received a B.Sc. in Physics from Purdue University and a M.Sc. in Industrial Administration from the Krannert Graduate School of Management.

Frank Findley is a data scientist and Executive Director of the Marketing Accountability Standards Board (MASB) where he represents the U.S. in the creation of international (ISO) marketing standards. His previous work at ARS group, comScore, and MSW Research resulted in improvements to ad testing, tracking, media planning, and competitive intelligence systems. He is a coinventor of the patented Outlook media planner. Findley’s research has appeared in numerous publications including the Journal of Advertising Research, Quirk’s, Forbes, and the books Accountable Marketing (Routledge, 2016) and Master of Marketing Measurement: Margaret Henderson Blair on Marketing Accountability (Cambridge Scholars Publishing, 2021). He was presented the 2021 ARF Great Minds Award for Best Practitioner Paper. He is a regular speaker at marketing industry conferences and a participant on industry boards. Findley received a B.Sc. in Physics from Purdue University and a M.Sc. in Industrial Administration from the Krannert Graduate School of Management.

Jim Meier served as MASB Director (2013-2018) and was appointed Trustee and Treasurer of the Marketing Accountability Foundation in 2019. He graduated from Marquette University in 1984 with a Bachelor’s degree in Accounting. After eight years as an auditor with Ernst & Young, he spent 26 years with Philip Morris, Miller Brewing Company and MillerCoors in financial support roles across Corporate Financial Services, Sales, Integrated Supply Chain, and Marketing. In his final role, VP Commercial Finance, Jim reported directly to the CFO and on a dotted-line basis to the CMO and CSO. He was closely involved with annual marketing spending allocation, on-going assessment of marketing mix modeling, and application of ROMI principles in both the Marketing and Sales divisions. Most recently, Jim has been engaged in assisting startup companies connected with a venture capital fund.

Jim Meier served as MASB Director (2013-2018) and was appointed Trustee and Treasurer of the Marketing Accountability Foundation in 2019. He graduated from Marquette University in 1984 with a Bachelor’s degree in Accounting. After eight years as an auditor with Ernst & Young, he spent 26 years with Philip Morris, Miller Brewing Company and MillerCoors in financial support roles across Corporate Financial Services, Sales, Integrated Supply Chain, and Marketing. In his final role, VP Commercial Finance, Jim reported directly to the CFO and on a dotted-line basis to the CMO and CSO. He was closely involved with annual marketing spending allocation, on-going assessment of marketing mix modeling, and application of ROMI principles in both the Marketing and Sales divisions. Most recently, Jim has been engaged in assisting startup companies connected with a venture capital fund.